Marshall Financial Solutions

Protecting you - Saving you Time and Money

Shareholder Protection

Shareholders acquire shareholder protection insurance because they want to protect their welfare.

Shareholder protection insurance also helps other shareholders settle any future problems say for instance the death of one of the shareholders or when a holder gets a serious illness. The help means, the other shareholder will be provided with cash which can be utilized in buying the shares of the deceased or sick shareholder.

However, the most benefited people are the family members of the insured shareholder who will receive the inheritance intended for them and by the quickest means possible while avoiding disruption of the company’s business transaction.

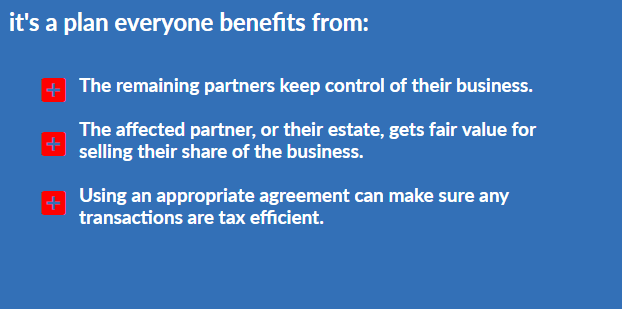

Shareholder Protection Insurance aims to protect not just the family and the affected shareholder himself, but the welfare of the entire company if selling and transferring take place. Shareholder protection insurance provides a lump sum amount of money (normally equivalent to the share value) in the event of a claim through death or critical illness.

With shareholder protection insurance the company takes out a life only or life & critical illness policy for each shareholder to the amount of their shareholding. In the event of a claim, the money is paid directly to the company in order to finance the purchase of the shares from the deceased next of kin. In order for this to happen smoothly, it is advisable to have a shareholder agreement in place which forces the next of kin to sell the shares back to the company. This is sometimes called a cross-option agreement.

Who'd be pulling your strings if your business partner died?

When a shareholder dies his or her shares will normally pass on to their husband or wife which in the case of many companies would not be ideal.

The consequences of this can be catastrophic for the company. For example the new shareholder may want to sit on the board and make detrimental decisions, or they may sell their shares to someone else not seen as a benefit to the other directors.

In the case of small partnership companies, loss of a 50% shareholder may mean a huge loss in profits and potentially end the company.

By putting shareholder protection in place, you could make sure the business gets the funds to buy back the shares from a critically ill partner or their estate.

![]() The Plan will have no cash in value at any time, and will cease at the end of the term. If premiums are not maintained, then the cover will lapse.

The Plan will have no cash in value at any time, and will cease at the end of the term. If premiums are not maintained, then the cover will lapse.